HSA Eligible Expenses Qualified Expenses for an HSA HSA Health Account ObamaCare Penalties for Those Without Insurance How ObamaCare Deals with HSA Plans and Your Children ACA: 3 Reasons to Choose an Off-Exchange Plan Delta Dental DeltaCare USA CAA54 Anthem Blue Cross of California Dental Select HMO Anthem Blue Cross of California Dental Blue Enhanced Delta Dental DeltaCare USA CAA55 Blue Shield of California Value Smile PPO Anthem Blue Cross of California Dental Blue Basic Humana of California Preventive Plus Dental Blue Shield of California Dental HMO Kaiser of California Dental Plan Rider Blue Shield of California Dental PPO Blue Shield of California Specialty Duo Dental and Vision Package ObamaCare: Federal Subsidies ObamaCare Bronze Plan Details Gold Plan Under ObamaCare ObamaCare Platinum Plan Outline ObamaCare Silver Plan Overview Child Health Insurance in California Finding an Affordable Health Insurance Company: Easy as 1-2-3 HSA Bank Account: Saving Health Insurance Dollars HSA Savings Account Maximum HSA Contribution What is an HSA? Affordable Health Insurance in Florida Individual Health Insurance In Florida HSA Contribution Limits How to find Affordable Child Health Insurance Understanding Affordable Self Employed Health Insurance Affordable Coverage Health Insurance: Easy as “ABC”

Knowing which procedures and items are HSA-eligible expenses is important for people with health savings accounts. In order to get the most benefit from an HSA, you’ve got to be prepared to use it on the wide variety of health-related expenses it covers.

HSA-eligible Expenses

While HSA plans have contribution limits, there are quite a lot of services you can use your contribution for. Here is a list of some of the things you can pay for with your tax-free HSA dollars include (but are not limited to):

* Abdominal supports

* Abortion

* Treatment for alcoholism

* Supports for arches

* Obstetrician

* Metabolism tests

* Costs associated with operating room

* Optician services

* Outpatient care lodging

* Neurologist

* Legal expenses

* Lab tests

* Ambulance fees

* Acupuncture

* Artificial limbs

* Blood transfusions

* Braces

* Cardiographs

* Blood tests

* Orthopedic shoes

* Oral surgery

* Nursing

* Osteopath

* Prescription birth control pills

* Optometrist

* Removal of lead based paint

* Transplantation of organs

* Spinal fluid test

* Radium therapy

* Handicapped schools

* Registered nurse

* Splints

* Psychologist

* Splints

* Prescription drugs

* Diathermy

* Elastic hose

* Eyeglasses

* Therapy for drug addiction

* Diagnostic fees

* Dentures

* Dermatologist

* Crutches

* Contact lenses

* Christian science practitioner

* Sterilization

* Fluoridation unit

* Surgeon

* Therapy equipment

* UV ray treatment

* Guide dog

* Treatment for gums

* Health care transportation expenses

* X rays

* Insulin treatments

* Wheelchair

* Hydrotherapy

* Hearing aids and batteries

These are only some of the HSA eligible expenses that are covered; with further research you may be able to uncover even more potential savings with this flexible health care tool.

Next, after you are signed up for the HDHP, you can then set up the actual health savings account at any financial institution that is qualified. This is much like opening an IRA or other investment vehicle. A bank or investment firm is the one that maintains the account. They will issue you an HSA debit card, probably with a Visa or Master Card logo on it and you can start spending your HSA dollars on HSA eligible expenses right away. As long as you continue to spend your funds on health-related expenses, they remain tax-free.

Shopping for an HSA

An HSA can be an excellent tool for a savvy family, but it’s not for everyone. The best way to find out if an HSA is right for you and your family is to get some hsa quotes, look at the premiums and evaluate the deductibles. Then you can decide whether the risk of the high deductible is worth the rewards of the low premiums, the tax-free savings, the flexible spending on health-related expenses, and the added control over how you spend your health care dollars.

To learn more contact us at 800-930-7956 or click here to get an HSA individual quote.

The great news about having a health savings account is that there are lots of qualified expenses for an HSA. Knowing which procedures and expenses are approved for tax-free withdrawals is important in order to maximize the use and benefit of your HSA account. If you live in California and were to purchase an Anthem Lumenos HSA California Plan this is the overview of coverage and costs.To get an idea of what medical items and services are considered eligible expenses for an HSA, have a look below. But keep in mind that this an example of what is included, not an exhaustive list.

Qualified Expenses for an HSA: A Sample List

* Abdominal supports

* Abortion

* Treatment for alcoholism

* Supports for arches

* Obstetrician

* Metabolism tests

* Costs associated with operating room

* Optician services

* Outpatient care lodging

* Neurologist

* Legal expenses

* Lab tests

* Ambulance fees

* Acupuncture

* Artificial limbs

* Blood transfusions

* Braces

* Cardiographs

* Blood tests

* Orthopedic shoes

* Oral surgery

* Nursing

* Osteopath

* Prescription birth control pills

* Optometrist

* Removal of lead based paint

* Transplantation of organs

* Spinal fluid test

* Radium therapy

* Handicapped schools

* Registered nurse

* Splints

* Psychologist

* Splints

* Prescription drugs

* Diathermy

* Elastic hose

* Eyeglasses

* Therapy for drug addiction

* Diagnostic fees

* Dentures

* Dermatologist

* Crutches

* Contact lenses

* Christian science practitioner

* Sterilization

* Fluoridation unit

* Surgeon

* Therapy equipment

* UV ray treatment

* Guide dog

* Treatment for gums

* Health care transportation expenses

* X rays

* Insulin treatments

* Wheelchair

* Hydrotherapy

* Hearing aids

Again, these are only some of the health care expenses that are covered. Others can be found by visiting the IRS website.

To take advantage of the flexibility, cost savings and tax advantages of an HSA, the first thing you must do is purchase an HSA-qualified insurance policy called a “high deductible health plan” or HDHP. The HSA and HDHP must always go together—they were designed by Congress to work as a pair. The upside of the high deductible part of the HDHP is that it generally makes your monthly premiums cheaper.

Next, when you have your HDHP policy started, you can then set up the actual health savings account at any financial institution that is qualified—usually a bank or investment firm. This is much like opening an IRA. You can choose a standard savings-type account, or can invest in bonds, stocks, or mutual funds if you like.

Once the HSA account is set up, you will receive an HSA debit card and/or checks. The HSA debit card is often branded with a VISA, Master Card or other such logo, making is easy to use in a variety of payment and purchasing settings. You can then start to use the HSA debit card on eligible expenses for an HSA. As long as the expenses are qualified, they remain tax-free. For more information call 800-930-7956 or click here to get an HSA quote.

HSA health accounts are more commonly known as health savings accounts or simply HSAs. HSAs function only in partnership with a specific type of health insurance plan called a High Deductible Health Plan. The two products—the HSA and the HDHP— combine to function as one health insurance distribution and payment plan. Together they create an affordable product with additional benefits for the consumer that extend beyond what is typically offered by a traditional health insurance plan alone.

The HSA/HDHP duo was created by an act of Congress. It replaced the medical savings account and started with the Medicare Prescription Drug, Improvements and Modernization Act that was passed into law on December 8, 2003.

HSA Minimum and Maximum Limits

There are specific amounts that you can contribute to your HSA each year. 2016 HSA Limits

HSA

2016 Limits

Deductible

$1,300/$2,600 (ind/fam)

Contribution

$3,350/$6,750 (ind/fam)

Max Out of Pocket

$6,550/$13,100 (ind/fam)

2015 HSA Limits

HSA

2015 Limits

Deductible

$1,300/$2,600 (ind/fam)

Contribution

$3,350/$6,650 (ind/fam)

Max Out of Pocket

$6,450/$12,900 (ind/fam)

Growing Money Tax-Free with an HSA Health Account

The best part about an HSA is that if you have a healthy year and don’t spend all the money in the account, it transfers to the next year. It is your money to keep and the total amount in your account can keep growing, year after year—it is the annual contributions that are capped, not the total amount in the account. So unlike other, lower deductible plans, you get to keep any savings and you get to control how you want your insurance money spent. Don’t confuse this plan with health reimbursement plans where you lose it at the end of the year if you don’t use it. It’s yours forever and can transfer to your family if there’s a balance when you pass.

The money in your HSA health account, like any health premium, is tax deductible and the money in the HSA grows tax-free as long as you use it only to pay for medical expenses. If you remove or use any funds for non-medical expenses and you’re younger than 59 A,A?, you’ll pay a federal tax penalty.

The HSA is Flexible

The tax code allows you to use your HSA money for such diverse items as dental treatment, alternative medicine like acupuncture, and some over-the-counter remedies. However, your insurance company that carries the high deductible health plan may not recognize these payments toward your deductible if they don’t allow payment for them in their plan. See our page on HSA Qualified Expenses to get an idea of what you can spend your HSA dollars on. Because the list of HSA qualified expenses is fairly diverse, you may not need a separate prescription drug plan, dental, or vision care plan, which is another way that having an HSA can save you money on health insurance premiums.

The health savings account is one of the best opportunities to save money on health insurance if your medical bills don’t normally meet your deductible amount each year. The high deductible plan often has a very inexpensive premium that saves money. For healthy individuals and families, the savings you achieve will often more than cover the amount of money a plan with a lower deductible would pay. For more information call 800-930-7956 or click here for a Health Savings Account (HSA) quote.

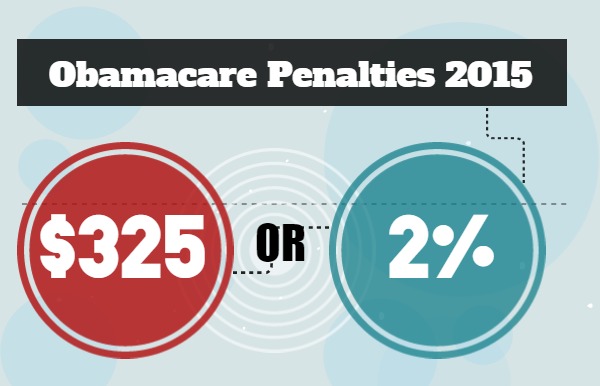

ObamaCare guarantees issuance for all regardless of preexisting conditions and therefore will impose a penalty for those that do not have insurance for the “metal” plans: Bronze Plan, Silver Plan, Gold Plan, and Platinum Plan.

How are Penalties Determined?

With the Affordable Care Act, penalties are determined by the amount of months that a person is without health insurance. For instance, if you didn’t have health insurance for 6 months a prorated amount will be tacked on when you do your taxes (you pay 50%). There are small windows of time that you go without insurance that will not effect you. Click here to learn about ObamaCare: Temporary Exemptions for the Uninsured.

What are the Federal Penalties for Being Uninsured?

$325 or 2% of your income in 2015, whichever is higher. There is also an uninsured child penalty of $162.50 per child, maxing out at $975 per family. To learn what your specific monthly premium under the Affordable Care Act would be call 800.930.7956.

Are there Federal Exemptions from Penalties?

Yes, there are a few ways to be exempt from a penalty:

You are an undocumented immigrant

Minimum coverage would exceed 8% of your income even after applied subsidies and/or employer contributions

Being without insurance for less than 3 months

Being below the poverty line, low enough that you don’t file a tax return

Against your religious beliefs

You are in jail or prison

You are a member of an Indian tribe

Americans who live abroad for at least 330 days a year

Further Questions

For any further questions about Obamacare penalties call 800.930.7956 or contact Medicoverage.

As you may have heard HSAs are here to stay, even with the new Affordable Care Act plans. But what does this mean for you children? Well, even though the new HSA plans must meet all the rest of the ACA rules, there is one that can affect your children.

Children and HSAs

Per the ACA all children up to 26 are able to stay on their parents’ health plan, however this does NOT apply to HSAs. Why, you may ask. It’s because HSAs are a tax thing, therefore the IRS still has jurisdiction and the IRS has not updated its age limit for a dependent.

IRS HSA rules for Dependents

If a person can’t claim their child as a dependent they can’t use their HSA funds to pay for them. The following is the IRS definition of who qualifies:

Resides in the same place as the covered employee for more than one-half of the taxable year.

The child has not provided more than half of his or her own support during the taxable year.

Is not yet 19 (or, if a student, not yet 24) at the end of the tax year.

Child is permanently and totally disabled

Could be biological child, adopted, stepchild, sibling, stepsibling, or descendant of

HSAs have Contribution Limits

There are very specific guidelines and rules for HSA contributions each year. Even though there are specific guidelines you will always want to check with your individual plan for any other rules or limitations that may apply (such as a higher deductible than the HSA min deductible).

To learn about plans available now for your dependent or to enroll in a new ACA plan call 800-930-7956 or contact Medicoverage.

The Health Insurance Marketplace’s virtual grand opening is October 1, 2013. However, many people don’t realize that the Exchanges aren’t the only game in town. You are able to purchase off-Exchange plans as well as the Affordable Care Act Bronze plan, Silver plan, Gold plan, and Platinum plans. We’ve listed 3 reasons why an off-Exchange may be the right choice for you.

1) Off-Exchange May Offer More Coverage

Off-Exchange plans are both grandfathered plans (plans enrolled in prior to March 23, 2010) and plans that are not purchased through the Health Insurance Marketplace. The main reason to purchase an on-Exchange plan is if you qualify for ObamaCare premium subsidies and/or federal cost-sharing subsidies. If you don’t qualify though, you might find a better value in plans offered off the Exchange. The reason for this is off-Exchange plans may be able to offer extra benefits not found on the Exchange, as well as they may offer lower premiums.

2) Off-Exchange Plans Save You Time

An Exchange plan takes a long time to gather all of your financial paperwork, as well as the time to fill out the application. If you know you don’t qualify for subsidies then you can save time by purchasing an off-Exchange plan.

3) Off-Exchange Plans Protect Your Privacy

Part of that paperwork you need to gather for apply for Exchange plans are your W2, child support, alimony, assets financial statements. This information is put out there. So, again, if you know you don’t qualify for subsidies, might as well protect your privacy with an off-Exchange plan.

Remember an agent or a navigator can help you with the on-Exchange plans, but only agents can help you with your off-Exchange plans. To learn more about plans outside of the Exchange or for the new metal plans call 800-930-7956 or contact Medicoverage.

Delta Dental offers the DeltaCare USA CAA54 for California. The CAA54 offers cleanings every six months at $20 each, however use the Delta Dental quote to get a plan overview such as a doctor finder, premiums, and a breakdown of costs for you and your family.

Basic DeltaCare USA CAA54 Details

Annual Deductible: None

Enrollment Fee: $10

Annual Maximum: Unlimited

Diagnostic Services: No Cost -$10

Preventive Services: No Cost -$85

Minor Services: No Cost -$85

Access To Providers: Network Providers Only

Major Services: $10-$495

Endodontics: $10-$725

Periodontics: $64-$650

Prosthodontics: $24-$700

Orthodontics: No Cost -$2,800

Any further questions call 800-930-7956 or for specific plan details you can locate the brochure through the DeltaCare CAA54 quote.

Anthem Blue Cross of California offers the Dental Select HMO plan. It includes free cleanings every six months, however use the Anthem Dental Select HMO quote to get details such as your premium, a doctor finder, and a cost breakdown.

Basic Anthem Blue Cross CA Dental Select HMO Details

Benefits

Annual Deductible: None

Enrollment Fee: None

Annual Maximum: Unlimited

Diagnostic Services: No Charge

Preventive Services: $5

Minor Services: $0-$187

Access To Providers: Network Providers Only

Major Services: $36-$223

Endodontics: $289-$459

Periodontics: $72

Prosthodontics: $432

Orthodontics: Child: $2,870/Adult: $3,045

Anthem Blue Cross of California Dental Blue Enhanced offers preventive services at $5. To learn about the plan’s complete details use the Anthem Blue Cross of California Dental Blue Enhanced quote to discover specifics such as your premium, a doctor finder, and a cost breakdown.

Basic Anthem Blue Cross CA Dental Select HMO Details

Benefits

Annual Deductible: None

Enrollment Fee: None

Annual Maximum: Unlimited

Diagnostic Services: No Charge

Preventive Services: $5

Minor Services: $0-$187

Access To Providers: Network Providers Only

Major Services: $36-$223

Endodontics: $289-$459

Periodontics: $72

Prosthodontics: $432

Orthodontics: Child: $2,870/Adult: $3,045

Delta Dental offers the DeltaCare USA CAA 55 California. You’ll find the most by getting a Delta Dental quote, you’ll get more details than below, such as a doctor finder, premiums, and a breakdown of costs for you and your family.

Annual Deductible: None

Enrollment Fee: $10

Annual Maximum: Unlimited

Diagnostic Services: No Cost -$10

Preventive Services: No Cost -$85

Minor Services: No Cost -$85

Access To Providers: Network Providers Only

Major Services: $10-$495

Endodontics: $10-$725

Periodontics: $64-$650

Prosthodontics: $24-$700

Orthodontics: No Cost -$2,800

Any further questions call 800-930-7956 or for specific plan details see the brochure through the DeltaCare Quote.

Blue Shield of California Value Smile PPO plan offers $0 preventive care including a complete set of X-rays. For a complete plan overview use the Blue Shield CA Value Smile quote tool to learn about your premium, find in-network doctors, and a cost breakdown.

Blue Shield of California Value Smile PPO Details

Annual Deductible: $25

Enrollment Fee: None

Annual Maximum: $500

Diagnostic Services: No Charge

Preventive Services: No Charge

Minor Services: $37 - $74

Access To Providers: Dentist of your choice

Major Services: Not Covered

Endodontics: Not Covered

Periodontics: Not Covered

Prosthodontics: Not Covered

Orthodontics: Not Covered

For further questions call 800-930-7956 or for specific plan details you can locate the brochure through the Blue Shield Value Smile PPO quote.

Anthem Blue Cross of California Dental Blue Basic is $0 preventive care before the deductible is satisfied. To see benefits at a glance use the Anthem Blue Cross of California Dental Blue Basic quote to find your specific premium, find doctors within in your network, and a cost breakdown.

Anthem Blue Cross of California Dental Blue Basic Overview

Annual Deductible: $25

Enrollment Fee: None

Annual Maximum: $500

Diagnostic Services: No Charge

Preventive Services: No Charge

Minor Services: 20%/40%

Access To Providers: Dentist of your choice

Major Services: Not Covered

Endodontics: 50%

Periodontics: Not Covered

Prosthodontics: 50%

Orthodontics: Not Covered

Humana of California offers Preventive Plus a PPO dental plan. All preventive care is $0, including one set of x-rays, however for a plan details use the Humana CA Preventive Plus quote to learn about your premium, find in-network doctors, and a cost breakdown.

Humana CA Preventive Plus Details

Annual Deductible: Individual $50/Family:$150

Annual Maximum: $1,000

Minor Services: 50%

For further questions call 800-930-7956 or for specific costs and details you can locate the brochure through the Humana Preventive Plus quote tool.

Blue Shield of California offers the Dental HMO plan. It includes $18 fillings, however for a plan overview use the Blue Shield CA Dental HMO quote tool to learn about your premium, find in-network doctors, and a cost breakdown.

Blue Shield of CA Dental HMO Basic Details

Benefits

Annual Deductible: None

Enrollment Fee: None

Annual Maximum: Unlimited

Diagnostic Services: $0-$13.00

Preventive Services: $0-$13.00

Minor Services: $18 - $23

Access To Providers: Network Providers Only

Major Services: $125 to $300

Endodontics: $155-$475

Periodontics: $75-$303

Prosthodontics: $400

Orthodontics: Adult $2,650/Child $2,350

For further questions call 800-930-7956 or for specific plan details you can locate the brochure through the Blue Shield Dental quote.

Kaiser of California Dental Plan Rider-only offers $54 X-rays. For a benefits at a glance use the Kaiser of California Dental Plan quote to find your specific premium and a cost breakdown.

Kaiser of California Dental Plan Rider Basic Details

Annual Deductible: $25

Annual Maximum: $1,000

Preventive Services: Adult: $43.20/Child $33.60

For further questions call 800-930-7956 or for specific plan details the brochure is available through the Blue Shield Value Smile PPO quote link.

Blue Shield of California offers the Dental PPO plan.The plan offers $0 preventive care, however for a complete plan overview use the Blue Shield of California Dental PPO quote tool to learn about your premium, find in-network doctors, and a cost breakdown.

Blue Shield of CA Dental HMO Basic Details

Annual Deductible: $50

Enrollment Fee: None

Annual Maximum: $1,000

Diagnostic Services: No Charge

Preventive Services: No Charge

Minor Services: $37 - $263

Access To Providers: Dentist of your choice

Major Services: $113- $320

Endodontics: $156-$234

Periodontics: $52-$210

Prosthodontics: $388

Orthodontics: Adults $2,650/Child $2,350

For further questions call 800-930-7956 or for specific plan details you can locate the brochure through the Blue Shield CA Dental PPO quote.

Blue Shield Specialty Duo Dental and Vision Package is offered in California.The plan offers $0 preventive care, however for benefits at a glance use the Blue Shield of California Specialty Duo Dental and Vision Package tool to learn about your specific monthly premium, find in-network doctors, and a cost breakdown.

Blue Shield CA Specialty Duo Dental/Vision Basic Details

Annual Deductible: $50

Enrollment Fee: None

Annual Maximum: $1,000

Diagnostic Services: No Charge

Preventive Services: No Charge

Minor Services: $37 - $263

Access To Providers: Dentist of your choice

Major Services: $113 to $320

Endodontics: $156-$234

Periodontics: $52- $210

Prosthodontics: $388

Orthodontics: Adults $2,650; Child $2,350

For further questions call 800-930-7956 or for specific plan details you can locate the brochure through the Blue Shield CA Dental/Vision quote.

Under ObamaCare there are federal subsidies to help with a portion of your health insurance under the new law. When the new Healthcare Exchange begins January 2014, with the new Bronze Plan, Silver Plan, Gold Plan, and Platinum Plan, there are two types of federal subsidies available: 1) Premium Subsidies, and 2) Cost-sharing Subsidies (coinsurance, copayments, deductibles).

What are Federal Premium Subsidies?

Federal Premium Subsides are available to help with the cost of month premiums, to help individuals and families have health coverage.

How it works:

You are eligible for a subsidy if you fall between 100 -400% of the Federal Poverty Line (FPL)

Depending on age and which plan the federal government will allot a portion of your premium

What are Federal Cost-Sharing Subsidies?

Federal Cost-Sharing Subsidies help with copayments, coinsurance, and deductibles for families that need extra help.

How it works:

You are eligible for a cost-sharing subsidy if you fall between 100 -250% of the FPL

If you have a Silver Plan -as this is the only plan eligible

Further Questions

To learn if you are eligible for either Federal Premium Subsidies or Federal Cost-Sharing Subsidies call 800-930-7956 or contact Medicoverage.

ObamaCare’s Healthcare Exchange begins January 1, 2014. All new “metal” plans must cover the same ObamaCare essential benefits, however this allows each state and/or provider to interpret the essential benefits in order to offer additional or extended coverage. The Bronze Plan has an actuarial (means this value may change dependent if you fall below 400% of the Federal Poverty Line (FPL)) value of 60%, which means that after your deductible has been met you pay 40% of medical expenses. Bronze is set up to have the lowest monthly premium*, with the highest out-of-pocket costs (combination of copayment, deductible, and coinsurance). Click here to compare Bronze Plan, Silver Plan, Gold Plan, and the Platinum Plan side-by-side.

Below is the most up-to-date information available, as the federal and state governments work to fine tune the details of these plans we will update this article.

*California was the first to release its Healthcare Exchange details and much of information we know so far is based on their figures. CHART UPDATED 9/26/13. For information about specific details of the Bronze health plan in your state call 800-930-7956.

UPDATE 11/27/13: For an easy way to fill out your Affordable Care Act application go to Healthapplication.com. Remember to fill it out and send it in as soon as possible to ensure the earliest enrollment date.

How Much is the Bronze Premium?

Premiums depend on age, state, provider, region, and whether you qualify for a federal premium exchange subsidy. With California’s numbers being the first available their average Bronze plan for a 21 year old is $177 without subsidies, but can be as low as $5 a month, and their average Bronze plan for a 40 year old is $226, and may go as low as $1 a month.

Comparing Bronze Plans to Other Metal Plans

The Bronze Plan will offer the lowest monthly premium, however you will pay the most in shared costs if you get injured or have a major medical issue.

Open enrollment period is from October 1, 2013 to March 31, 2014. For questions about the Bronze Plan in your state please contact Medicoverage.

The Affordable Care Act (ACA), commonly known as ObamaCare, begins its Healthcare Exchange January 1, 2014. The open enrollment for these plans begins October 1, 2013 and ends March 31, 2014, and each plan must offer of ObamaCare essential benefits. Although every plan across the country must offer these benefits, states and providers may still offer additional or extended coverage. The Gold Plan has the 2nd highest monthly premium, but the second lowest cost-sharing costs. Click here to compare Bronze Plan, Silver Plan, Gold Plan, and the Platinum Plan side-by-side.

Below is the most up-to-date information available, as the federal and state governments work to fine tune the details of these plans we will update this article.

Gold Plans*

These Gold plans are specific to individual and family members. Click here to learn about how the Gold plan applies to ObamaCare Small Businesses.

Benefits

Gold Health Plan*

Deductible

$0

Preventive

$0

Doctor’s Office Visits

$30

Specialist

$50

Generic Rx

$19

Brand RX

$50

Lab Testing

$35

X-ray

$50

Maternity

$600 per day HMO**/20% PPO

Out-patient Surgery

$600 HMO/20% PPO

Hospital Stay

$600 per day HMO**/20% PPO

ER Visit

$250

Urgent Care

$60

Out-of-Pocket Max

$6,350/$12,700 (ind/fam)

**up to 5 days

*California was the first to release its Healthcare Exchange overview, and much of information we know so far is based on their figures. CHART UPDATED 9/26/13. For information about specific details of the Gold Plan in your state call 800-930-7956.

UPDATE 11/27/13: For an easy way to fill out your Affordable Care Act application go to Healthapplication.com. Remember to fill it out and send it in as soon as possible to ensure the earliest enrollment date.

How Much is the Gold Premium?

Premiums depend on age, state, region, provider, and whether you qualify for a federal premium exchange subsidy. With California’s numbers being the first available, the lowest Gold Plan for a 40 year old, non-smoker living in Los Angeles is approximately $276.

Further Questions

For questions about the Gold Plan in your state please contact Medicoverage.

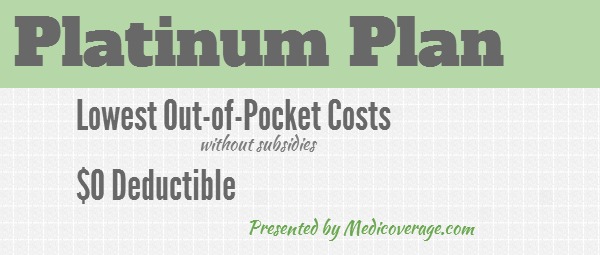

ObamaCare begins its Healthcare Exchange as of January 2014. Each new “metal” plan must offer the Healthcare Exchange essential benefits. Although every plan must offer these benefits, states and providers may still extended or add additional benefits to these plans.The Platinum Plan has the highest monthly premium with the lowest out-of-pocket costs. Click here to compare Bronze Plan, Silver Plan, Gold Plan, and the Platinum Plan side-by-side.

Below is the most up-to-date information available, as the federal and state governments work to fine tune the details of these plans we will update this article.

Platinum Plans*

These Platinum plans are specific to individual and family members. Click here to learn about how the Platinum plan applies to the Healthcare Exchange and Small Businesses.

Benefits

Platinum Health Plan*

Deductible

$0

Preventive

$0

Doctor’s Office Visits

$20

Specialist

$40

Generic Rx

$5

Brand RX

$15

Lab Testing

$20

X-ray

$40

Maternity

$250 per day HMO**/10% PPO

Out-patient Surgery

$250 HMO/10% PPO

Hospital Stay

$250 per day HMO**/10% PPO

ER Visit

$150

Urgent Care

$40

Out-of-Pocket Max

$4,000/$8,000 (ind/fam)

**Up to 5 days

*California was the first to release its Healthcare Exchange details and much of the copay information we know so far are based on their figures. CHART UPDATED 9/26/13. For information about specific details of the Platinum health plan in your state call 800-930-7956.

UPDATE 11/27/13: For an easy way to fill out your Affordable Care Act application go to Healthapplication.com. Remember to fill it out and send it in as soon as possible to ensure the earliest enrollment date.

How Much is the Platinum Premium?

Premiums depend on state, region, provider, age, and whether you qualify for a federal premium exchange subsidy. With California’s numbers being the first available, the lowest priced Platinum Plan for a 40 year old, non-smoker living in Los Angeles is $311.

Next Steps:

For questions about the Platinum Plan in your state please contact Medicoverage.

Below is the most up-to-date information available, as the federal and state governments work to fine tune the details of these plans we will update this article.

*California was the first to release its Healthcare Exchange overview, and much of information we know so far is based on their figures. CHART UPDATED 9/26/13. For information about specific details of the Bronze health plan in your state call 800-930-7956.

UPDATE 11/27/13: For an easy way to fill out your Affordable Care Act application go to the ObamaCare Exchange Healthapplication.com. Remember to fill it out and send it in as soon as possible to ensure the earliest enrollment date.

How Much is the Silver Premium?

Premiums depend on provider, age, state, region, and whether you qualify for a federal premium exchange subsidy. With California’s numbers being the first available their average Silver plan for a 21 year old is $191 without subsidies, but can be as low as $41 a month, and CA’s average Silver plan for a 40 year old is $226, and may go as low as $37 a month depending if you qualify for a subsidy.

Comparing Silver Plans to Other ObamaCare Plans

The Silver Plan will offer the second lowest monthly premium, however it is the only plan that allows for cost-sharing subsidies if you qualify.

The initial enrollment period for the Healthcare Exchange is from October 1, 2013 to March 31, 2014. For questions about the Silver Plan in your state please contact Medicoverage.

The famous “SCHIP” (aka the State Children’s Health Insurance Program) law was enacted to provide health insurance to children in low-wage, working families who would otherwise be uninsured. If you do not meet California’s definition of “low income,” you will need to find child health insurance in California. We can help.

Selecting a Plan for Your Child

Perhaps the most cost-effective way to get child health insurance in California is to cover your child as a dependent under your own insurance plan—this is especially true if your plan is paid in part of in full by your employer. Ages vary by state, but in general your child can remain covered under your plan up to a certain age—often 19—after which point they must enroll in their own plan. This age is higher if your child is a full time student and/or if you can claim them as a dependent on your tax return. Again, this varies by state so you should research this separately, and then verify your child’s dependent status with a licensed tax professional.

If covering your child as a dependent under your plan is not an option, you will need to find them an individual health insurance plan. This can be done in 3 simple steps.

Research Online. Go to our online health quote tool here and type in your child’s zip code at the top of the page. You’ll get a list of plans for child health insurance in California. From there you can quickly and easily look at what each plan offers versus the price they charge to see which plan suits your child’s needs best.

Refine. Now look specifically at those things that will both save you money and get your child the best care. For instance, make sure the plan you choose covers immunizations if your child hasn’t had them all yet (they can be expensive and add up!); or if your child is on medication, make sure the plan covers prescription drugs. Also make sure you’re not paying for things you don’t need: your 7-year-old son can do without that expensive maternity coverage and tobacco cessation program.

Use wisely. Once you enroll in a plan for your child, use it wisely. For example, can you solve your child’s immediate health concern with a free after-hours phone call to the on-call pediatrician instead of an expensive trip to the emergency room? Or did you know that you can shop around for medical procedures and that prices can vary quite a bit for the exact same treatment? Be a savvy consumer and you can save money and still receive good care.

Paying for your Child’s Health Insurance

Many parents do not know that they can continue to help pay for their child’s health insurance, in part or in full, indefinitely. Simply set up your credit card, bank account or billing address, instead of theirs, for payment.

Just about everyone wants to find a quality health insurance plan, but finding an affordable health insurance company can seem like a difficult and complicated task. Contrary to popular belief, however, there is not one insurance provider that is more affordable than the rest. Most insurance companies offer dozens of health insurance plans ranging from more basic, lower cost plans to higher-end, more expensive ones.

3 Steps to Finding the Right Insurance Company

Step 1: Consider size. An affordable health insurance company should have enough members to negotiate the best rates with doctors. More members mean more bargaining power, which in turn tends to mean better rates. Smaller insurance companies often have to pay higher fees for the same medical costs, and they pass those fees on to you.

Step 2: Compare plans online. With an online quote tool like ours at Medicoverage, you can quickly compare various health insurance companies and their plans until you find one that matches your needs. If you purchased CoreShare Plus Colorado this is your breakdown of costs and coverage. Click here and enter your zip code at the top of the page to get a list of easy-to-compare quotes in 10 seconds or less. This online research will allow you to select a plan with only the services you need and avoid paying extra fees for services that you don’t use (e.g. maternity if you are a man).

Step 3: Check quality. Do a little research into the company before you select one of their plans to ensure that they have excellent feedback and ratings from other customers. It won’t matter how cheap the insurance is if you can’t get good care when you need it.

Saving After You’re Covered

There are some common sense things you can do after you have health insurance that can continue to save you money on medical care

Before you get any treatment, shop around for the best price. The cost for the same procedure can vary dramatically.

Only go the emergency room when necessary.

Try home remedies.

Use existing x-rays when you go to the dentist.

Use mail order prescription drugs.

Purchase generic or over the counter drugs when possible.

Choose a plan with a higher deductible, which saves you money on monthly premiums.

Pay for your premiums once a year, as this is often cheaper than monthly.

Use your local free clinic for basic services, even if you have insurance, these can save you money if you are in a tight financial spot .

Using the tips above, you should be able to find an affordable health insurance company and, more importantly, a health insurance plan that suits both your health and your finances.

An HSA bank account in combination with a high deductible health plan (HDHP) is one of the savviest new forms of health insurance. Congress gave the American public an opportunity to save money while still getting excellent health insurance when they passed the bill allowing for the Health Savings Account (HSA).

Traditional health insurance costs thousands of dollars in premiums every year. Many healthy insured don’t receive much benefit from those plans, or not enough to cover the cost of high premiums. HSA-qualified HDHPs, however, have high deductibles but relatively lower premiums. The trade-off they do require higher out-of-pocket expenditures up front. Most people fear that they won’t have the funds available if they should have an accident or become ill and require expensive medical treatments. If you were to purchase an Anthem Lumenos HSA Connecticut this is an overview and explanation of costs and coverage.

The HSA/HDHP combo, however eliminates the subscriber’s exposure to such catastrophic risk because once the individual or family has met their deductible, the insurance company kicks in its payments. So for run-of-the mill doctor’s appointments and prescription medications, you’ll generally foot the bill, but if things go really wrong, the insurance company takes on that financial risk. The great part is that if you and your family have a healthy year and don’t use the money you’ve socked away in your HSA bank account, it just rolls over to the next year, tax-free. And it can keep growing and growing, year after healthy year.

Setting up an HSA Bank Account

Once you enroll in an HSA-qualifying HDHP health insurance plan, you can then set up your HSA. You can do this at major banks like Bank of American and Wells Fargo, or use the bank associated with your health insurance plan. Once the plan is set up, you usually receive a debit card and checks just as you would for any normal checking account. You can use the money in the account to pay for your medical expenses that go toward satisfying your health insurance deductible.

Additionally you can also draw upon the account for more types of expenses than your high deductible plan allows. If you need eyeglasses or dental work, services health insurance policies don’t usually cover; you can use the funds from the HSA and still maintain the tax-free status for those funds. Of course, these cost do not apply toward the deductible on your health plan.

When selecting an HSA savings account, you should make sure to check their fees and interest rate. We have found that currently the interest rates on most HSAs are low but you should be able to select a plan that will offset any banking fees.

HSA Bank Account Restrictions

HSA savings accounts do have some restrictions. For instance, in the year 2010, individuals under the age of 55 can contribute a maximum of $3,050 to the an individual HSA. Families can contribute up to $6,150 to a family HSA. However, if you’re 55 or older, you can to add an additional $1,000 to the account every year as a catch-up provision of the plan. Even if you start the plan later in the tax year, you can still contribute the full amount as long as your coverage began the first day of the last month of your taxable year. If you’re like most people and use the calendar tax year, that date would be December 1.

HSA Out of Pocket Maximums and Minimum Deductibles

There are also some rules that apply to the HDHPs that must be enrolled in alongside the HSA bank accounts. Those are the out-of-pocket maximums and the minimum deductible. The maximum out-of-pocket expense, including deductibles, that participants can be required to pay is $5,950 for individual coverage, and $11,900 for family coverage.

The minimum deductible of the high-deductible health insurance plan to which HSAs must be linked is $1,200 for single coverage and $2,400 for family coverage.

Remember, if you don’t use the money in the account, it rolls over to the following year for later use. It’s yours to keep forever. Even if you pass away, your heirs receive the funds. If you go on Medicare, you no longer can contribute to the HSA. However, you still can use the remaining funds for medical purposes. The premium on long-term care insurance is one of the options allowed. Eye glasses, alternative medical procedures and even payments for vitamins all qualify as medical expenses. Have a look at our HSA Expenses page to get an idea of all the things you can pay for with an HSA bank account.

If you want a way to save money on the cost of your health insurance, consider a Health Savings Account, or HSA for short, and a high deductible health plan, or HDHP for short. The health savings account is a flexible savings vehicle designed for those that want to take control over their medical spending. Note that if you decide to establish an HSA, you must also elect an HDHP for your health insurance coverage—the two function as a pair. Congress created the HSA/HDHP combo in an effort to give consumers greater control over how they spend their health care dollars. Simply put, you establish an HSA with a financial institution, typically a bank, deposit a certain amount of money in the account each year, and then spend that money via the bank’s debit card on health-related expenses. See our HSA Contribution Limits page for information on how much you can put into your account each year.

The dollar amount in the HSA savings account coordinates with the insurance plan’s deductible, but also gives you a lot more benefit than simply paying expenses to meet that deductible. For instance, because the HDHP by definition has a high deductible, it will in turn have relatively lower monthly premiums than most traditional health insurance plans. Also, you can use your HSA debit card to pay for health-related expenses that many traditional health care plans typically would not cover. If you purchased an Anthem Lumenos HSA Virginia health plan this is your overview of benefits and costs. See below for examples.

HSA for Dental and Vision Expenses

Individual vision plans are often inadequate or have limited coverage and most often simply include discounts. Dental insurance is often expensive and offers a limited reimbursement toward larger bills. By using an HSA savings account and high deductible health plan, instead of purchasing vision or dental insurance, you can use the funds you accumulate in your tax-free savings account toward the cost of dental and vision care needs.

Using an HSA Plan

Once the money is in your account, you control how you spend it. If you want to pay for a medical expense that your insurance company doesn’t cover, such as certain “over-the-counter” medicines , you can use your HSA. The insurance company may not count these expenses towards satisfying your deductible, but it will reduce your overall cost as these purchases will be made with tax free dollars. Learn more about how you can use your health saving account at our HSA qualified expenses page.

Health Savings Account as a Savings Vehicle

If you don’t use the money in the HSA savings account, it remains yours to keep. And while there are limits on how much you can contribute to your health savings account each year, there are currently no limits as to how much you can allow to accumulate there—tax tree. That’s the best part! You no longer have to pay high premiums to insurance companies only to end up with no claims at the end of the year and money out the window. The unused HSA funds transfer to the following year and continues to grow interest and accumulate until you need it. It remains yours forever. Use for medical needs most companies refuse to cover if you wish or continue to accumulate funds. At death, it passes to heirs. You don’t have to pay the money into your HSA savings account all at once or on a systematic basis. If you find that you have a lump sum you’d like to add in addition to the amount you already contribute monthly, you can do it as long as it doesn’t go over the maximum amount set by the federal government.

Health Savings Accounts for Employers

In addition to all the benefits described above for individuals, HSA savings accounts and high deductible health plans can also be used by employers. If you, as an employer, can’t offer complete health coverage, you may contribute to employees HSA accounts but you must make certain that you offer the same amount to each employee if you do it on a pretax basis in order to comply with non-discrimination rules. To learn more about how to use or set up a health savings account for a small business, visit our Small Business HSA page.

HSA Maximum Contributions Typically Increase Each Year

If you have an HSA (Health Savings Account) and an HDHP (High Deductible Health Plan), you need to be aware that the maximum HSA contribution increases every year as the cost of living increases. Because of this, the plan is ideal as a way to save money on your health care insurance. If you don’t have an HSA and HDHP, it may be a good idea to consider this often overlooked option for your health care coverage. For example, if you live in Missouri and were to purchase an Anthem Lumenos HSA Missouri plan, this is an explanation of benefits and coverage.

If you wish to use an HSA, you must elect a qualified HDHP. The HSA - HDHP combination allows you to control how you spend your health care dollars. Also, when you use the HSA savings account with a high deductible health plan, any money growing tax-free in your account that you did not use in the current year can simply roll over into the next year, allowing you to grow a substantial sum over time.

2009 Maximum Contribution

The maximum HSA contribution for individual plans for the year 2009 was $3,000. However, if you’re over the age of 55, you can tuck away an additional $1,000. The maximum HSA contribution for family coverage was $5,950. You don’t have to be part of the plan all year in order to get the benefit of the tax-deductible health plan. If you start a plan as late as the first day of the last month of the taxable year, you can take the maximum HSA contribution for the year.

2010 Maximum Contribution

The maximum contribution that can be made to an HSA in 2010 for individuals is $3,050, up from $3,000 in 2009. The maximum HSA contribution for those with family coverage rose to $6,150 from $5,950.

Out of Pocket Maximum

The maximum out-of-pocket expense, including deductibles, that HSA subscribers can be required to pay in 2010 is $5,950 for single coverage, up from $5,800 in 2009 and $11,900 for family coverage, up from $11,600.

Minimum Deductible

The minimum deductible for the high-deductible health insurance plan to which HSAs must be linked has increased in 2010 to $1,200 for individual coverage and $2,400 for family coverage. These figures are up from $1,150 for individual coverage and $2,300 for family coverage in 2009.

HSA Pro and Cons

On the con side, the high deductible insurance plan may seem at first as though you don’t have insurance at all because you keep paying bills until you meet your deductible. But on the pro side, remember that the money you put into the health savings account should cover the deductible amount, and that money is not taxed. Plus, as mentioned previously, if you don’t use it, you keep it and it continues to grow for your future use. The more you accumulate, the less you worry about an out-of-pocket amount for any type of medical need. The really big pro here is that if you or a family member develops a catastrophic illness, you let the insurance company bear the risk and burden of the higher bills you accrue.

Rules for HSA Spending

Just like any plan that offers you the ability to grow dollars on a tax-free basis, there are rules. If you remove the money from your health savings account for any expense that’s not health related; you pay a penalty to the IRS. The really good news is that the health savings account rules allow you to use it for a variety of different health-related expenses—not just what a typical insurance plan would cover. For example, if you wish to use the money in the HSA savings account for dental procedures, something your health insurance typically wouldn’t pay, you have the option to use it without penalty for that purpose. Have a look at our list of qualified expenses to get an idea of what you can use your HSA to pay for.

The HSA is a Flexible Health Insurance Tool

The HSA account is extremely flexible and really puts you at the helm when it comes to spending health care dollars. And each year as the maximum HSA contribution increases, it adds more benefit to those savvy consumers that select the health savings account and high deductible health plan as their form of insurance protection.

If you’ve heard the term “HSA” on television or read it in financial articles, you may wonder, what exactly is an HSA? The acronym HSA stands for Health Savings Account. The HSA is a special type of account that allows the account owner to store money in a tax-free vehicle, and then use that money to pay for health related expenses.

The Health Savings Account was created by Congress to help make health insurance more affordable by giving consumers more direct control over and visibility of how their health insurance dollars are spent. The idea is that, if a consumer puts his or her own money into this specially-designed savings account and then spends it on health services, then they will know exactly where that money goes. For a person living in Ohio, the Anthem Lumenos HSA Ohio plan explanation of benefits page helps explain why an HSA might be right for you.

HSA as a Savings Account

One really unique and potentially beneficial feature of the HSA is it’s potential for saving money tax-free. The idea here is that the money you put into an HSA does not get taxed by the IRS at the end of the year. Then, if you have a healthy year and do not spend all the money in your HSA, that money is yours to keep and roll over to next year. Don’t forget that the money in that account may also earn a bit of interest if you have it in an interest-earning account, though interest earnings on HSA accounts tend to be quite small.

How Does an HSA Work?

The total HSA package has two parts. The first part is the health saving account discussed above and the second part is the HDHP. HDHP stands for “High Deductible Health Plan.” If you want to take advantage of an HSA, you must enroll in a high deductible health plan. By definition, a HDHP has a high deductible, which means that you will be responsible for paying all of your medical expenses out of your HSA until you meet the deductible amount. The HDHP minimum deductible for 2010 is $1,200 for individual coverage or $2,400 for family coverage.

To put this into an everyday example, here’s how the deductible would work. Let’s say you have an HSA with a high deductible health plan and are the head of a family of four. You will pay for all of your doctor visit bills, prescription medication bills and any trips to the emergency room up until you have paid a total of $2,400. Once you reach that point, your insurance company starts to kick in it’s contribution toward paying your bills, with some exceptions depending on the individual plan. Most policies have a co-payment until you reach the out of pocket maximum. The co-payment is the percent of the bill you pay. You can use the funds in the health savings account to offset this also. Keep in mind that the deductible resets each year. This means that in 2011, your contributions toward your deductible reset back to zero. (This is true of all health insurance plan deductibles, not just HSA-compatible HDHPs.)

HDHP plans typically have a relatively lower monthly premium to offset the high deductible. Also to offset the high deductible, the HSA funds are tax-deductible and grow tax-deferred.

HSA Qualified Expenses

But watch out. If you use the funds for something not medically related, you’ll pay a penalty to the IRS. Suppose you wanted a new big screen television and used the HSA to buy it. It doesn’t matter if it makes you feel better, it’s not medically necessary and you’ll pay a penalty. Check out our list of HSA qualified expenses HSA qualified expenses to get an idea of what you can pay for with an HSA.

HSA Contributions

Once the plan is in place, the insured can currently contribute up to $3,050 or the amount of the deductible if it’s an individual plan. If it’s a family plan then the maximum amount allowable for contribution is $6,150. That is, unless the insured is 55 years old but not yet on Medicare. In this case, the tax code allows for an additional $1000 per year contribution. If you have the plan in place by the 1st day of the last month of the taxable year, you can contribute the entire amount and receive the tax deduction. It’s a great tax-planning tool.

Additional HSA Benefits

There are additional benefits besides tax planning and lower payments for insurance. One of them is how you use the money in the HSA account. Many insurance policies don’t cover prescription drugs, eye care, or dental. Since these are all medically related expenses, the government allows you to use the money in an HSA to pay for these without triggering a penalty. That means you can pay for all of these expenses tax-free when you otherwise would not be able to under many other traditional health plans.

You also get to keep any money that you don’t use that year and roll it into the next year. This is a wonderful way to increase the funds and allow you to save even more by increasing the deductible on your health insurance policy. If you don’t spend the money in the account, it’s yours to use as you choose at retirement. Of course, you have to pay tax on the growth if you later decide to spend it on non-medical expenses.

Now you Know!

Now when someone asks, “What is an HSA?” you can tell them it’s a cost effective method of securing quality health insurance, building assets and directing the money for health care the way you think it needs to be spent.

Despite the fact that it really is possible to find affordable health insurance in Florida, there are well over 3.5 million uninsured individuals in the Sunshine State. That’s almost 24% of the state’s population walking around without health insurance coverage, which is well over the national average of 17.4%. These high numbers may be attributed to Florida’s 8.1% unemployment rate, which ranks higher than the national average. Many unemployed people face the high cost of COBRA, or may not even have COBRA as an option if their former employer has shut down. However, nearly a million people in Florida have discovered that there are affordable health care plans available online, and that applying for these plans can actually be a much simpler and faster process than they’d expected.

Do I Really Need Florida Health Insurance?

Some young, healthy individuals think that they do not need insurance because they don’t take prescription medication, see the doctor, or have any major health issues. This is risky behavior for several reasons. First, nobody plans to get sick or have an accident and it is impossible to predict when you or a member of your family could need urgent medical help. More than 12 million Americans are rushed to the emergency room each year for accidents alone. Of these, over 22% are otherwise healthy people with serious sports or recreation-related injuries. And if you apply for health insurance after you are sick or injured, many Florida health plans will turn you down based on your pre-existing condition. Second, medical bills are expensive and the uninsured pay the highest rates for health care. This is because health insurance companies pool their members into a big group and then negotiate much lower rates for health services on behalf of their members. If you’re not a member, you don’t get their negotiated rate. And in some cases that non-negotiated rate can be as much as FIVE TIMES higher than the negotiated rate. Finally, being uninsured is financially very risky. According to a 2007 study, 62% of all personal bankruptcies in America were due to medical bills individuals or families simply could not pay.

Get Informed About Health Insurance in Florida

If you aren’t one of the Floridians covered under a public or private health plan, you need to know that there are other options available that can meet your needs and your budget.

Public Assistance

One thing to consider when looking for affordable health insurance in Florida is whether you qualify for any sort of public assistance. People who are below a certain income level can usually qualify for this assistance, as long as they meet a certain criteria. While the insurance that you receive might not be the best in the country, it will certainly be better than having no health coverage at all. Check Florida’s state government website for information.

Individual / Family Health Insurance

One of the best options around is for you or a member of your family to be offered health insurance that is paid for in part or in full by your employer. If that is not an option for you, or if you are self-employed, you will need to shop for what is called individual or family health insurance. In order to save money on health insurance in Florida and find the best match for your personal or family health care coverage needs, you’ll need to compare different plans offered by different health insurance providers and see the price quotes offered by each plan. Visiting a general site like Medicoverage allows you to do just that so you can choose from a broad range of Florida health insurance companies and see how their plan rates and benefits stack up against each other. When you visit a site like that, the only required fields should be for zip code, gender, birth date, and possibly smoking status. This site and many others also may ask for contact information, but this should be optional. Also, no site can truthfully advertise that they offer lower prices on specific plans than any other site. By Federal law, no website or insurance broker can offer any one plan at a lower price than any other website or broker. In other words, if it is the same plan offered by the same health insurance provider, it can only be sold at the same price, no matter who is selling it.

Getting Started Finding Affordable Florida Health Insurance

Because things can sometimes take a turn for the unexpected, finding affordable health insurance in Florida should be at the top of the savvy person’s to-do list. Though it’s not free, being insured in Florida is a less risky decision in the long run—for both your health and your finances. The guidance at Medicoverage.com is easy to understand, plus it offers plenty of simple advice on health insurance and a quick and easy quote engine to get and compare Florida health insurance plans in as little as 10 seconds. Click here to try the Medicoverage quote engine.

Although many think of it as a myth, there really is such a thing as affordable individual health insurance in Florida. However, if you were to look at the statistics, you would no doubt assume that this is yet another urban legend. More than 20% of Florida residents have no health insurance and about 25% of Florida’s workforce does has no medical coverage. Since the state is home to over 6 million uninsured workers, it’s hardly surprising that interest in the proposed health care reform being debated by the federal government is at an all-time high.

Why are so many Floridians uninsured?

There are many different answers to this question, but most uninsured people in the state say that they don’t anticipate becoming ill (of course, most people don’t), or that they have no idea where they can find affordable individual health insurance in Florida. While it may be difficult to convince someone that they are not, in fact, invincible, there are some simple ways to find affordable health coverage in Florida.

Starting with Individual Health Insurance

An individual health plan is different and separate from any health insurance plan provided by your employer. An individual health plan is one you purchase on your own, and it can be a lot less expensive than group health insurance. Since the insurer is not obligated to sell you a policy, you may find it difficult to buy coverage if you have one or more preexisting conditions. The premiums (which are the monthly ‘dues’ you’ll pay) for individual plans are typically calculated based on anticipated medical costs. Typically older people, overweight people and smokers will tend to pay much higher premiums than younger, healthier people.

Finding the Right Individual Health Plan

There are a couple of things to think about before you start looking for an affordable health insurance plan in Florida. For example, would you like to stay with your current physician? If so, then you should probably look for a PPO plan. These plans usually allow you to see any physician you choose, but you’ll want to find a plan which includes your doctor as a preferred provider. You can simply call your doctor’s office and ask which insurance plans they accept before you choose your plan. However, if you choose an HMO plan, then you’ll have to use the HMO’s physician network.

The next thing to think about is the cost of your premiums and out-of-pocket expenses under the plan. Out-of-pocket expenses are the costs which you must pay for first before your insurance company kicks in to pay for medical expenses. Generally speaking in Florida, the higher the out-of-pocket expenses, the lower your premiums and vice-versa. If you frequently need to see your physician and take prescription medications regularly, then opting for a plan with a higher premium and lower out-of-pocket expenses makes sense; you’ll often find these plans offered by HMOs. However, if you’re in good health and only see your physician rarely, you’ll likely do better with a PPO plan which features higher out-of-pocket expenses and lower premiums.

Where to Start

Finding individual health insurance in Florida that fits into your budget starts with knowing what you need from your medical plan. You’ll also want to know where to search efficiently for coverage. A great place to start is a website like www.medicoverage.com, where you’ll find a Florida health insurance quote engine. One quick search will pull up dozens of results for insurance plans from some of Florida’s top insurance companies. With a little shopping around and some research, you’ll discover that affordable health insurance really does exist in the Sunshine State.

A Health Savings Account (HSA) allows you to set aside pre-tax money qualified medical expenses, but there are certain certain HSA contribution limits, which you’ll see listed below. This tool is available to you as a taxpayer if you are enrolled in what’s called a High Deductible Health Plan and if you use the funds in your HSA account only for qualified medical expenses. The HSA tax advantage works because you are not subject to federal income tax on the amount of money you put into the account. Unlike other types of accounts offered, these funds can roll over year after year, so that you can accumulate the funds for medical emergencies and other expenses, if necessary. You, the individual, own these funds as well, which is different than past health care payment funds. If you purchased an Anthem Lumenos HSA Colorado plan, this is an explanation of contribution limits, benefits, and costs.

Background:

With HSA funds, you can pay for qualified medical expenses without having to pay federal taxes on them. Similar to withdrawals from an IRA, you are penalized if you withdraw them for use that is not qualified under the plan—i.e. you use funds to pay for non-medical expenses or non-approved expenses. These accounts are part of what’s sometimes referred to as “consumer driven health care.” They were established as part of the Medicare Prescription Drug, Improvement and Modernization Act signed into law by President George W. Bush in 2003. HSAs were meant to replace the Medical Savings Account system, which were the types of accounts previously used as a means to pay for medical expenses by consumers.

HSA contribution limits and other rules of use:

As with IRAs, HSAs do have rules for use. You must be enrolled in a tax-qualified, HSA, high-deductible health plan. There is an advantage to making pretax contributions, because FICA and Medicare tax deduction savings can amount to 7.65% each to the employer and employee.

Contribution limits

There are limits to how much you can contribute to your HSA during the year. There are also minimum required plan deductibles and caps on out-of-pocket maximums for HSA-approved plans. The limits are listed below.

2016 Individuals / Families

Maximum Contribution $3,350 / $6,750

Minimum Deductible $1,300 / $2,600

Out-of-Pocket Maximum $6,550 / $13,100

2015 Individuals / Families

Maximum Contribution $3,350 / $6,650

Minimum Deductible $1,300 / $2,600

Out-of-Pocket Maximum $6,450 / $12,900

Investing funds:

You can invest HSA funds similar to the way you can invest individual retirement account funds. These earnings are not subject to taxation until you withdraw the money, and if the withdrawal is to pay for a qualifying medical expense, they remain not taxable. You can roll over HSAs from fund to fund, but you cannot roll them into an IRA or 401(k). Similarly, you cannot roll funds from an IRA or 401(k) into HSAs.

Investing through an employer:

If you invest through an employer, the funds will belong to you immediately, regardless of who deposited them. In addition, you don’t have to contribute to an employer-sponsored HSA, unless you want to.

Withdrawing HSA contributions:

You may withdraw HSA funds for qualified medical expenses at any time without being subject to federal taxes on that money. However, if you withdraw the funds for any other purpose, they may be subject to penalties or taxation.

Finding affordable health insurance for your child can seem like a daunting task, but with some key information at your fingertips, it can be very doable. The majority of parents buy health insurance for their kids right after the infant is born. You may be surprised to discover that the rates are very high for newborns. This article will address some techniques get your child covered and save money.

Key Tips to Help You Save Money

1) It is important to know that you cannot purchase health insurance until your baby is born. The good news is that under the Newborns’ and Mothers’ Health Protection Act, your infant can be covered under the mother’s current health plan for the first month after birth. Look to see if this is relevant to you before you give birth. This additional month of coverage gives you the chance to carefully search for a plan that fits your family’s requirements.

2) While rates are typically very high during that first year of coverage, you will be glad to know that after age one, the monthly rate for the child lowers significantly. The trick is to make sure that your child is over 1 year old on the anniversary month of his or her new plan. This is complicated but it’s very important to understand. Here is an example: Let’s say your child was born on September 13 and you purchase health insurance for him or her on September 29. His/her health insurance anniversary month is September. The problem occurs because s/he will still be under 1 year of age on September 1 when the policy renews. You will then be charged another year at the higher under-1-year-old rate. Yes, the entire year! This higher cost for the second year could be avoided if you started his new plan any time in October.

3) The first years of life are important for your little one and a preventative health care schedule should be implemented. You can accomplish this by selecting a good pediatrician for your baby and maintaining your baby’s schedule of well-baby visits. When looking for an affordable child health insurance plan, be sure to confirm that immunizations are covered under these well baby visits, as there will be plenty and they are critical to your child’s health and safety. Some plans do not offer immunization coverage until after the deductible is paid. Your savings on a so-called A>?,?_"low costA>?,?A_ plan my not be realized because such a plan will require you to pay for those vaccinations yourself and they can be expensive.

4) Another method to save money is to not buy maternity coverage for your baby. Since your kid will not be having a baby for a long time, it makes sense not to buy this benefit. If you are adding you child to your existing plan, but know this is your last child, you may want to remove maternity from your coverage as well.

5) As you may know, health insurance plans have various coverage selections. Because most healthy kids do not often require taking costly brand-name prescription medications, it may be fitting for you to select a plan that has a high deductible for brand-name prescription drug coverage. This will save you money, yet still provide you with brand-name coverage in the event that you do need it.

There are many affordable insurance plans out there for babies and children. Your next step is to look for a quote for your child and use some of the methods mentioned above to help you save money once you select a plan. Visit our home page to get a quote for your child now (insert link to home page)

In this guide, you will gain a general understanding of health insurance for someone who is self employed.

You’re On Your Own

The economy remains in turmoil and each day thousands of individuals around the nation lose their jobs through layoffs, terminations, and business closures. Unfortunately when these jobs are lost, it means more than just a loss of income, stability, and self-esteem… it also means a loss of medical coverage. Many individuals who have suffered the effects of the tough economy have discovered that self employment is the way to go. Getting your own business off the ground is a great accomplishment and a good way to start bringing in income, but you’ll quickly discover that when you’re self employed, you’re on own when it comes to getting health insurance.

There Is No Difference Between “Self Employed” Insurance and “Individual” or “Family Insurance”

First and foremost, you must understand that there is no difference between health insurance for those who are self employed and health insurance for and individuals and families. There are no special prices or treatments just because your status is self employed. Please be very wary of anyone offering “special insurance” only for those who are self employed or of someone asking you to join their “self employed network” so you can gain special discounted coverage.

Using Insurance Quote Engines

As your own employer, the best strategy you can use to get health insurance is to search via an individual and/or family health insurance quote engine to get a sense of the prices associated with insurance providers in your area. For instance, if you live in California one of the most popular health insurance plans is Anthem Premier Plus California. Our quote engine is here. You can think of our quote engine (and others) as an “Orbitz for health insurance.” Our online tool (and most others) only require a small amount of information and return a large number of results. You are typically only be required to enter your birthday, gender and your zip code to get an accurate quote. Once you have answered all the inquiries posed by a given quote tool, it will return results that highlight companies available as well as health coverage plans that detail policy specifics and pricing. In order to ensure that you get the best plans for your needs, most results include the following key information:

1) Name of Plan and Provider

2) Monthly Premium

3) Annual Deductible

4) Co-payment or Co-insurance amounts

You can also click into the plan summary to understand key details such as out of pocket maximum and lifetime payout. A telephone number is also provided so you can speak directly to representatives that can answer questions and assist you in finding the best coverage for your needs.

Pre-Existing Conditions

If you have medical conditions that are considered to be “pre-existing,” you may run into some difficulty finding a policy that accepts you. It is important to become familiar with the laws that govern your state to determine if there is a clause for what is referred to as “Guaranteed Issued Health Insurance.” While this type of coverage is often not as inclusive as other types, it will provide you with basic coverage for your health care needs.

Speaking With an Agent

If after using the quote engines, you still find that acquiring health insurance is a challenge, it may be time to seek the assistance of an authorized agent that can help you locate the medical coverage that’s right for you. Visit our contact page to choose the best way to get in touch with a Medicoverage agent (insert link to contact page). When you’re self employed, understanding all the steps to successfully finding health insurance may prove to be challenging, but it really can be done. All it takes is a little know how.

It’s not as difficult as you may think to find affordable coverage health insurance; just follow my “ABC” recommendations below.

A) Avoid benefits that look good on paper but don’t actually save you money

The first step to finding health insurance that meets your budget, steer clear of benefits that you won’t really save you that much money. This may seem counterintuitive, but there are some health services that you may need from time to time but would prefer to not have covered as part of your health insurance plan. One example of this is the very popular $5 co-pay for physician’s office visits. This is one of those things which looks great on paper, but remember that this means that you’ll be paying a much higher monthly premium for your coverage - and office visits don’t tend to be all that costly. For instance if you purchased Anthem CoreShare Plus Virginia you would have a plan that has a low monthly premium, while covering you in case of major medical issues.

B) Buy only health coverage that you’ll actually use

The next trick we recommend is to avoid plans with benefits that you won’t really need or use. For example, if you’re a man, you can safely skip maternity coverage in your health insurance plan.

When you’re looking for affordable coverage health insurance, the same rule applies to other benefits. Another example is no-deductible coverage of brand name medications. Brand name drugs are far more costly than their generic equivalents. Particularly for young people who don’t need prescription drugs on a regular basis, it’s not usually worth the hundreds of dollars per month that this coverage can cost. If you do go for a health insurance plan which includes brand name medication coverage, try to find a plan that has a separate brand name drug deductible; this will cost you far less.